Immediate Investment Authorization: Strengths and weaknesses in Mexico's new investment policy

On May 4, 2026, the Office of the President and the Ministry of Finance and Public Credit published three instruments intended to redefine public policy regarding productive investment and foreign trade: the Decree for the Immediate Investment Authorization, the Decree Establishing the Unique Platform for International Trade Procedures, and the General Criteria and Operational Guidelines for the Promotion of Productive Investment and Tax Compliance. In this post, we share the main points regarding these measures.

A Solution to the Structural Problem of Investment?

The Decree for the Immediate Authorization of Investments creates a novel mechanism in Mexico: the “Authorization” for the immediate implementation of investment projects. This mechanism aims to facilitate the launch of investment projects without bureaucratic costs and with simplified compliance with certain procedures. The central objective is to accelerate the start of operations for strategic projects, reducing the time associated with procedures involving the public administration.

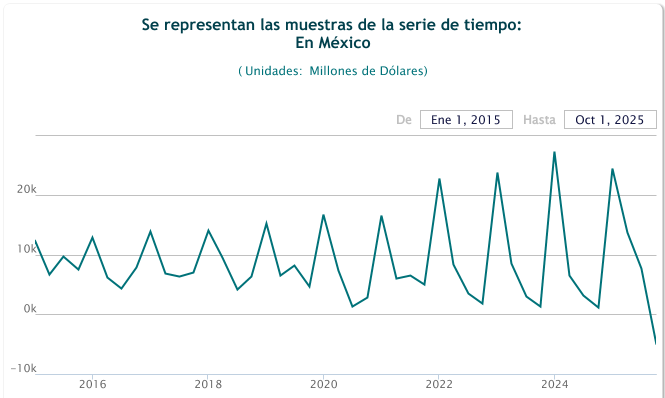

Source: Mexico’s Total Investment, Financial Information System from Mexico’s Central Bank

The creation of the immediate authorization mechanism responds to an adverse landscape facing productive investment in Mexico. In particular, Mexico’s productive investment fell by 44.9% in the first two months of 2026, the largest decline since this indicator has been measured. In addition, Mexico experienced a 6.8% decline in total investment in the country. This decline has particularly impacted investments in the energy and hydrocarbons sector. Therefore, the Mexican government has committed to promoting investment and reversing this trend.

Design of the Immediate Investment Authorization Scheme

The scheme applies to three broad categories of “investment projects”:

- Investments authorized to be developed Mexico’s Development Areas.

- Investments equal to or exceeding 2 billion pesos (approximately $115 million).

- Investments in strategic sectors such as:

- Semiconductors

- Automotive

- Pharmaceuticals

- Aerospace

- Energy

- Chemicals

- Textiles

- Medical devices

- Technology infrastructure

The mining and financial sectors are expressly excluded from these incentives, as are those constituting public or mixed-ownership investments. Investors must apply for the Authorization through the National Digital Investment Portal, submitting a dossier containing corporate and tax information, as well as a detailed project proposal covering technical, environmental, energy, water, and local supply aspects. In addition, the rules require a letter of commitment to contract domestic suppliers for at least 20% of the investment amount.

Once the application is approved, the Authorization is initially valid for one year and may be renewed up to two times. During its term, the investor may begin operations immediately and process the procedures included in the Authorization. The administration of authorizations falls to an Investment Committee, composed of the Ministries of Finance, Environment, Energy, Economy, and Anti-Corruption, and coordinated by the Presidential Office for Investment Promotion.

Immediate Investment Authorization: Regulatory Fast-Track or Selective Incentive?

While official discourse emphasizes facilitation and legal certainty, a closer analysis reveals structural limitations that call its effectiveness into question. The scheme applies to projects that: (1) have prior authorization to be developed in a Development Area, (2) involve investments of 2 billion pesos or more (approximately 115 million USD), or (3) fall within a strategic sector. This threshold excludes a significant portion of investment, as much of the foreign direct investment (FDI) in Mexico does not reach those capital levels.

From a practical perspective, the Decree is not designed to incentivize new investment, but rather to accelerate projects that have already passed prior screening or that, due to their size, already possess the capacity for regulatory management. Added to this is the fact that the Development Hubs lack significant tax incentives, which substantially reduces their appeal.

Furthermore, the Decree requires a complex technical dossier, which includes plans for energy, water, and gas consumption, waste generation, emissions, detailed timelines, and commitments to domestic sourcing. Furthermore, the Authorization has a limited term (one year, renewable), is subject to quarterly reports, and may be suspended or revoked in the event of formal non-compliance, delays, or additional criteria that the Committee itself may determine in subsequent regulations. In terms of legal certainty, the temporary benefit may prove insufficient in light of the latent regulatory risk.

Decree on the Unique Platform for International Trade Procedures: Institutional Advances with Operational Challenges

In contrast, the Decree establishing the Unique Platform for International Trade Procedures represents a more substantial step forward in terms of institutional design. By establishing it as the sole mandatory channel for processing procedures and centralizing its administration within the Agency for Digital Transformation and Telecommunications (ATDT, in Spanish), the system is provided with a framework for governance, interoperability, and traceability.

In addition, the creation of a Unique Foreign Trade Dossier; the reinforcement of the full validity of electronic notifications; and the emphasis on the authorities’ obligation to respect deadlines and legal requirements are elements that, if properly implemented, can reduce friction in import and export operations.

However, significant questions remain regarding the ATDT’s technical and operational capacity to assume functions previously handled by the SAT, as well as regarding the effective transition of the VUCEM without disrupting ongoing procedures.

General Criteria and Operational Guidelines for the Promotion of Investment

Finally, the Ministry of the Treasury issued general criteria and operational guidelines intended to promote productive investment and tax compliance. Essentially, this agreement seeks to signal greater openness, understanding, and flexibility in the oversight of investment projects. Furthermore, it prioritizes transparent action, such as adherence to the principle of non-retroactivity when applying review criteria.

To a large extent, these general criteria and operational guidelines respond to the growing concerns and complaints of certain investors. Recently, the National Foreign Trade Council (NFTC) filed a formal complaint with the Ministry of Finance regarding hostile treatment by the Mexican Tax Administration Service (SAT). Furthermore, this comes amid proposals to integrate the Taxpayers Ombudsperson (PRODECON, in Spanish) into the Ministry for Anti-Corruption and Good Governance, a move that would call its autonomy into question.

However, the general criteria and operational guidelines acknowledge their purely advisory nature, without implying a legal limitation or a mandatory practice for the SAT. For investors, this means that the rules of the fiscal game remain unchanged; rather, good intentions are stated, and compliance with them will depend on the discretion of each authority.

Final Remarks

Taken together, the various published instruments reflect a clear commitment to digitalization and administrative coordination, but they also confirm a public policy approach that prioritizes certain administrative streamlining only for projects that, due to their location or scale, favor the interests of the public administration. To attract investment in the current economic context, administrative speed alone does not compensate for the lack of tax certainty, clear incentives, and accessible rules for medium-sized projects.

For companies, the key will be to determine whether these investment promotion mechanisms represent a real strategic advantage or merely an alternative compliance route, with high regulatory costs and limited benefits.

More information?

VTZ is a Mexican law firm specialized in international trade and customs. Contact our key members:

Gilberto Mejia

Author

Emilio Arteaga

Jr. Partner